US yield curve is dynamic on election eve

Last Update: 25/12/2024

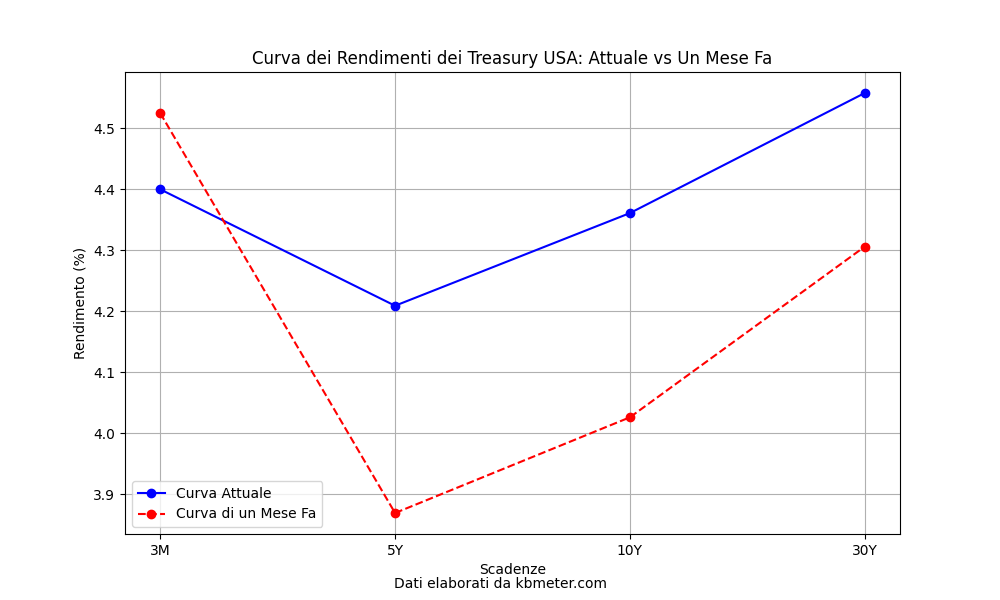

The US government bond yield curve is looking very “dynamic” in the hours leading up to the presidential election (tomorrow) and the FED meeting (Thursday).

In the chart above we look at what is happening at various maturities by comparing the current situation with that of a month ago. We note a reduction in yields on very short maturities accompanied by an upward acceleration in yields on long maturities. In other words, the movement seems to indicate an increase in the steepness of the long curve and a gradual reduction in the inversion present in the short end (0-2 years).

There are several possible causes of this movement. The most quoted at the moment has to do with inflation expectations in the long term, in part a child of speculation about the course of tomorrow’s elections. Yields on longer maturities incorporate an inflation risk premium; the higher the yield, the more likely it is that rising inflation scenarios are being discounted. Some analysts say that in that premium between short and long maturities there is also a share of risk associated with the health of U.S. government debt, which is at risk of deterioration if many of the election promises are kept.