The response of the S&P500 sectors to the U.S. election results

Last Update: 25/12/2024

After intense weeks for U.S. politics and the economy let’s take a look at how the 11 sectors that make up the S&P500 moved. A thermometer of investors’ expectations for the coming months.

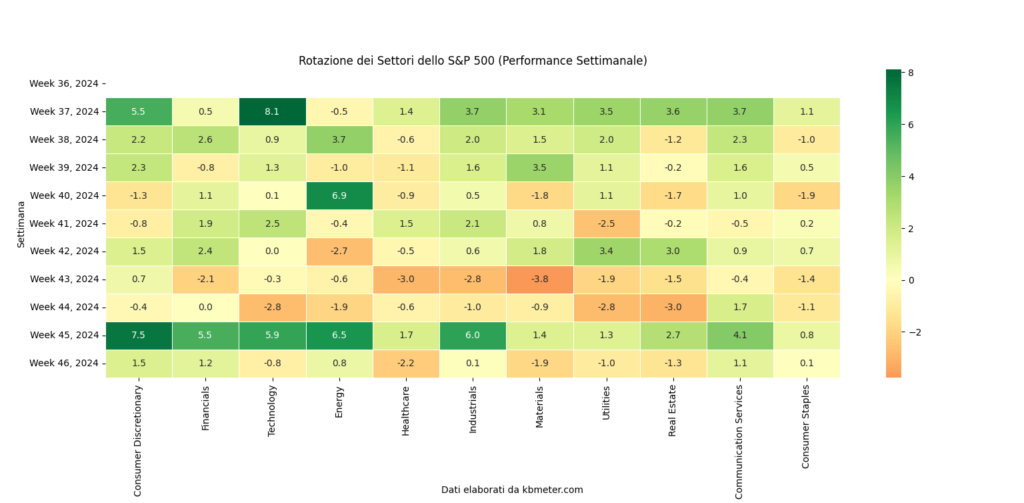

We start by showing the weekly returns of the S&P500 sectors through a heatmap. We see it below.

As noted, the “hottest” point occurred during election week. The main beneficiaries were consumer discretionary, financials, technology, energy, industrials and communications. With a cool head and a few more indications about the composition of the new Trump administration, investors have begun to make their choices: down utilities (abandoning defensives), real estate (on higher rates hypothesis and longer), pharmaceuticals (on the indication of Robert F. Kennedy Jr. as the new health minister).

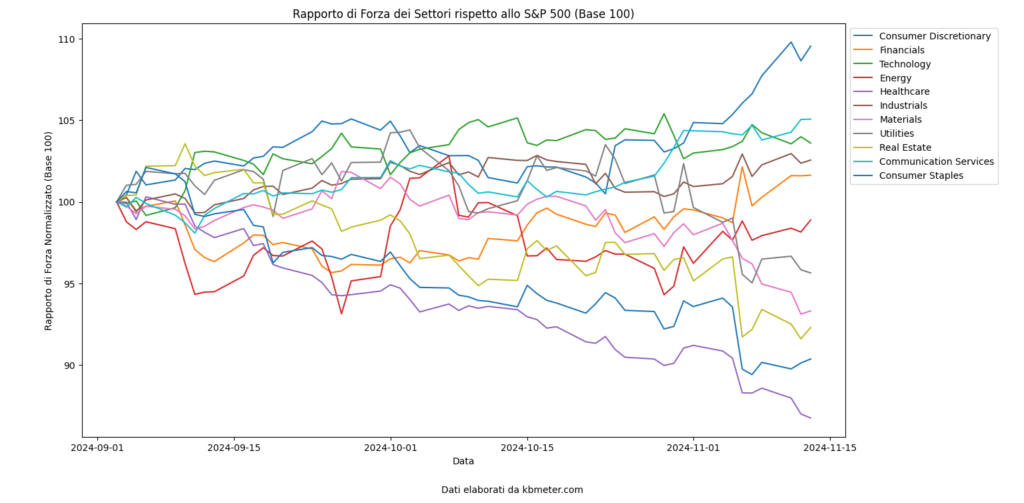

Looking at the trends in the strength ratios between the various sectors and the S&P500 index (figure above) shows the strong recovery of consumer discretionary (the blue line further up) and the burst forward of financials, while more moderate appear to be the gains in strength of technology and energy. Lagging behind are sectors such as utilities, consumer staples, pharmaceuticals and real estate.

This weeks’ rotation, indicative of increased risk-on, must of course be taken with caution. Already in the past, post-election choices have not been very good for investors. In 2016, for example, Trump’s first election, the energy sector was touted, but after four years it was found to be the index’s worst performer.