France, not just spreads, equities also lose strength

Last Update: 25/12/2024

It is a high-tension December for France, both in terms of the future of public accounts and the financial markets. Slowing economic growth and increased spending on social and energy policies to deal with inflation and the energy transition have pushed public debt to 114 percent of GDP in the second quarter of 2024.

The current political crisis only adds to investors’ uncertainty and nervousness. On the one hand, so-called “bond vigilantes” have pushed up French government bond yields and consequently the spread against German bunds. On the other hand, the stock market, in advance of the bond market, has also been sending signals about the less than brilliant health of the French economy.

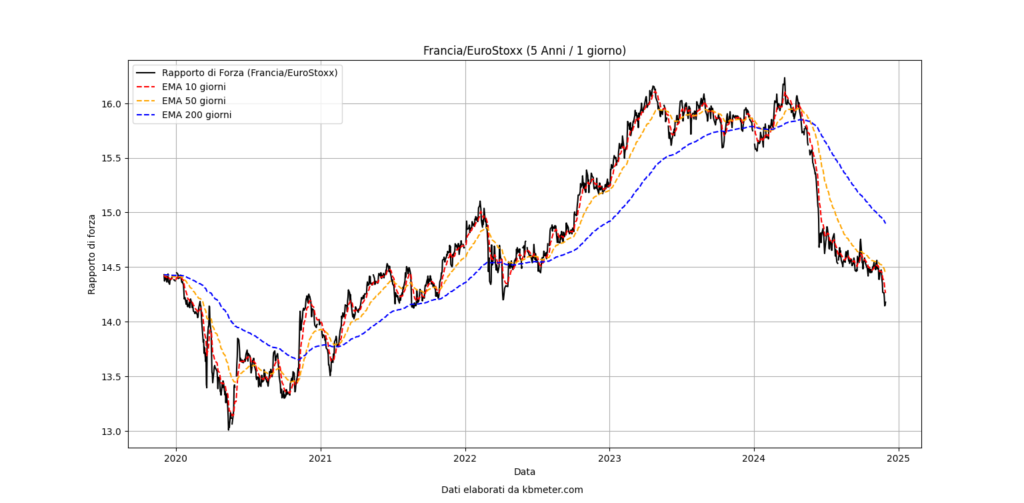

Above we see the trend in the strength ratio between the CAC 40, the French benchmark index, and the Eurostoxx 600. As can be seen, the performance of the Parisian list was better than the pan-European index from the end of the acute phase of the pandemic, until early 2023. Then, after a sideways period in early 2024, the CAC 40 began to lose strength, now arriving at early 2022 levels; well below the 200-day average.

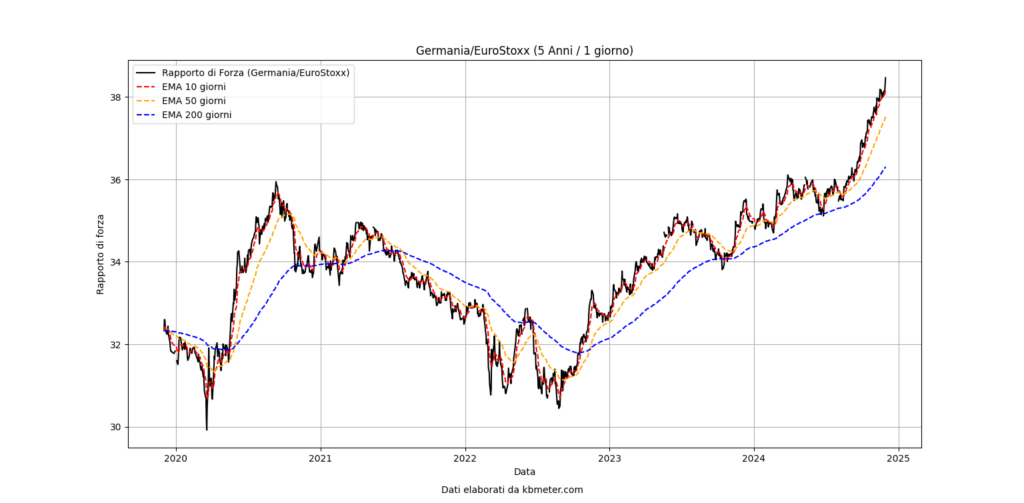

One interesting item is a comparison with the performance of the DAX versus the Eurostoxx over the same period. We see this in the figure above. We can see the positive pitch of the strength ratio starting in mid-2022 and strengthening from early 2024 onward.

The impression is that investors, among the two big sick of Europe, seem to have more comforting expectations about Germany. A rotation that has become decidedly more evident since early 2024.