Argentina, financial markets reward recovery efforts

Last Update: 25/12/2024

Although still in a delicate and in many ways dramatic situation, Argentina has embarked on a path of recovery that seems to be bearing fruit; and financial markets confirm.

The economic situation in Argentina remains extremely delicate. Key macroeconomic data seem to indicate a beginning of improvement, but the price of these small steps remain extremely high.

For the first time in 16 years, the government has achieved a budget surplus in the first six months of 2024, thanks to significant spending cuts and increased tax revenues. Annual inflation is forecast at 104 percent by the end of 2024 and on a monthly basis fell to 2.7 percent in October; the lowest since 2021. The economy contracted -1.7% in the second quarter of 2024, marking an improvement from the previous -5.1%, but remaining in a technical recession.

The achievement of these results, which are certainly important and necessary, also brings with it decidedly worrying numbers: interest rates at 35%, the drastic reduction in public investment (-80%) and local financing (-70%), the poverty rate reaching 52.9%, up 11 points since the beginning of the Milei government’s term, and the unemployment rate at 7.6% (almost two points higher than at the end of 2023).

A complex and delicate economic and social situation. Against this backdrop, however, the financial markets seem to be giving confidence in the path forward.

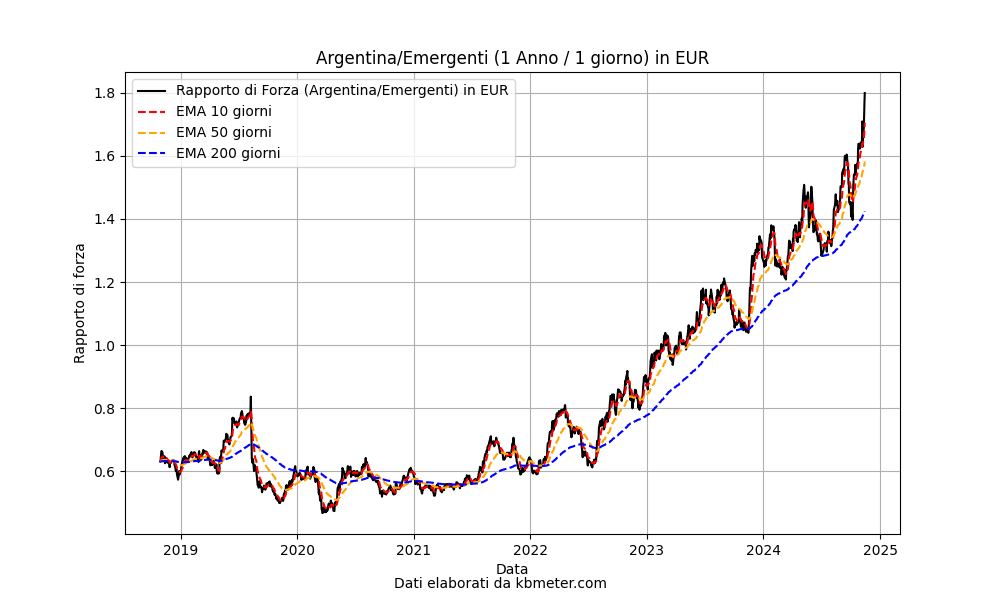

The graph depicted above represents the strength ratio between Argentina equities (via etf ARGT) and emerging economies equities (via ETF EEM). We can see the positive trend of the ratio from 2022 onward, with a significant acceleration from the second half of 2024.

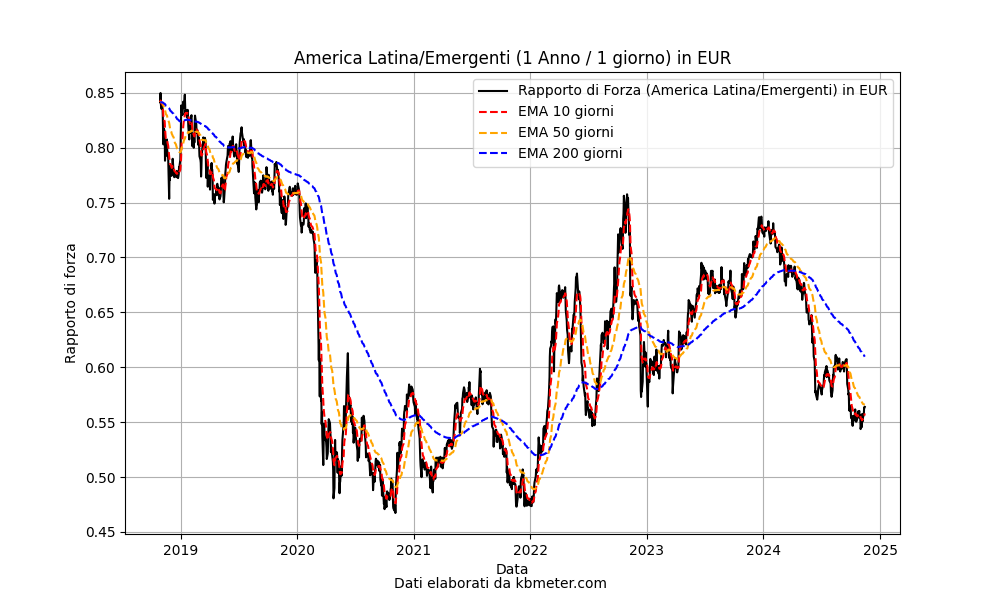

Over the same period (chart above), the relative strength of Latin American equities relative to the emerging economies as a whole has shown a markedly different pattern, with 2024 clearly struggling.